Table Of Contents

- What is margin in trading?

- What Does it Mean to Trade on Margin?

- What assets can you trade on margin?

- Why isn't margin trading free money?

- How does margin trading work?

- Practical Considerations When Trading on Margin

- Step-by-Step Guide to Buying on Margin

- Real-world Worked Example

- What are the key elements of margin trading?

- What should margin investors consider?

- What does “margin” mean outside trading?

- How can you manage risk in margin trading?

- What are the pros and cons of margin trading?

- What are the best strategies for trading on margin?

- Start slowly

- Practice with demo trading

- Don't keep positions open for too long

- Don't risk too much on each trade

- Set stop-loss and take profit levels

- Stay informed

- The Bottom Line

Top Facts Every Trader Must Know About Margin Trading

Margin trading is a fast-paced and exciting part of retail trading. In the financial landscapes of FOREX, cryptocurrencies, and other financial assets, margin trading has emerged as a potent tool for investors aiming to amplify their returns. However, with high potential comes high risk. It’s a balancing act for traders, as the promise of bigger gains comes with the potential for bigger losses.

In this article, I will explore margin trading, examining its risks and rewards, its mechanics, and how to utilize it in conjunction with sound investment strategies. I will also discuss which markets are best suited to margin trading. Like many investments, finding out if margin trading is for you will come down to how you feel about its pros and cons after conducting thorough research.

Margin trading lets you borrow funds from your broker to control larger positions using your existing capital as collateral

Leverage increases both profit potential and the size of possible losses which makes risk management essential.

If your account value drops below the broker’s maintenance requirement you will face a margin call requiring additional funds.

Margin trading is available across all asset classes

Successful traders typically limit risk to a small portion of their total capital per trade often no more than 1 to 2 percent.

Using margin effectively requires staying on top of market news economic reports central bank decisions and technical trends.

While margin offers opportunities like short selling or increased market exposure it also raises the risk of significant losses

Beginners must use demo accounts and follow a risk management plan before trading with margin.

What is margin in trading?

margin in trading is money you borrow from a broker to buy more financial assets than your own cash would allow. It acts as a loan that increases your market exposure and can amplify both gains and losses. This borrowing power is usually shown as a ratio, such as 2:1, meaning you can control twice the amount of capital in your account.

When trading on margin, you use your investment as collateral for the borrowed money. If the investment increases in value, you stand to gain more than if you had only invested your own money because you control a larger position. However, this comes with increased risk. If the investment decreases in value, you will lose more than if you had just used your own money.

Further, you still owe the broker the borrowed amount, and you may need to deposit more money to meet a margin call when your account hits a pre-determined stop out level. Traders should know that interest is usually charged on the borrowed money, and the terms can vary from broker to broker.

Additionally, not all securities can be purchased on margin (we will cover which ones later), and there are regulations that set minimum margin requirements.

Overall, while trading on margin has the potential to magnify profits, it also can amplify losses. You should only engage in it with a clear understanding of the risks and requirements involved.

What Does it Mean to Trade on Margin?

You start by depositing cash (or marginable securities) into a margin account. That deposit becomes the collateral for the loan. Look at the graphic that follows, based on an example with 30:1 leverage:

Trade Composition (Margin vs Borrowed Funds)

Margin is just a small deposit controlling a much larger position

The practical effect is extra buying power. Your deposit, combined with the loan, allows you to hold a larger position than you could otherwise. The securities you buy then automatically serve as further collateral for the loan, which is why brokers closely monitor your account value. If values fall, your equity shrinks, and you may face a margin call, in which the broker can liquidate positions to protect the loan.

Use margin deliberately. If the trade doesn’t beat the borrowing cost, you lose money faster.

What assets can you trade on margin?

Margin trading is available for many financial assets, though the exact types depend on your brokerage or trading platform. Here are some of the most commonly traded assets:

Stocks

Margin trading is most commonly associated with stock trading. Many brokerages allow their clients to borrow money to purchase more shares than they could with just their available cash.

FOREX

The FOREX market is another market where margin trading is actively used. Traders can take on prominent positions in currency pairs with relatively small amounts of capital, thanks to leverage.

Cryptocurrencies

With the rise of digital assets, many cryptocurrency exchanges now offer margin trading. This enables traders to amplify their trading positions in cryptocurrencies such as Bitcoin, Ethereum, and others.

Futures contracts

Futures are contracts that obligate the buyer to buy or the seller to sell an asset at a specified price on a future date. Many futures contracts are traded on margin, meaning that traders only need to deposit a fraction of the total contract value to take a position.

Options

Options are derivatives based on the value of underlying securities, like stocks. Buying on margin is not typically done with options, but selling options can be done on margin as long as you have an approved margin account.

Exchange Traded Funds (ETF)

These are investment funds traded on stock exchanges, similar to individual stocks. Some brokerages allow margin trading for ETFs.

Bonds

While less common than stocks or FOREX, some brokerages do allow margin trading for bonds. The investor can borrow money to buy more bonds than they could afford outright.

Commodities

Just like futures, commodities such as oil, gold, and agricultural products can also be traded on margin.

For traders, it’s essential to understand the risks associated with margin trading in these various markets. While the potential for higher profits is alluring, there is also the risk of substantial losses, particularly given the volatility of specific markets, such as cryptocurrencies and commodities.

Join a Trading Community That Moves Together

Follow top traders and learn from real strategies.

Like, comment, and engage with other investors.

Discover experts through transparent performance data.

Connect with a community built on trust and results.

Grow your knowledge while trading smarter together.

.webp)

Why isn't margin trading free money?

Margin trading is not free money because the borrowed funds must be repaid to the broker, usually with interest payments and possible fees. The loan remains an obligation even while you are using it to trade. Any gains you make do not cancel the debt, because the broker still expects full repayment.

As soon as you turn a profit, the broker's loan becomes due in full.

If you encounter losses early on, the broker can issue a margin call, requiring you to add funds or reduce positions to restore the required equity. The terms of the margin call also allow the exchange to assume ownership of any assets within your account.

Margin trading is a practice that requires active involvement. Many financial markets fluctuate constantly, making it doubly important to remain diligent and monitor your investments at all times.

How does margin trading work?

Margin is the equity you actually own in your brokerage account. Buying on margin means you top up that equity with money borrowed from your broker, but you need a margin account to do it, not a plain cash account. In practice, the broker lets you buy more assets than your cash would allow by using the cash and securities already in your account as collateral.

Margin only helps when you expect the investment’s return to outpace the interest you’re paying on the loan. Otherwise, the interest drag can turn a winning trade into a losing one.

Here's an explanation of a trade I carried out myself:

I had $200 of my own cash in a margin account, and I used it to buy $1,000 worth of stock. That meant my total exposure was $1,000, even though only $200 of it was my own money. The broker lent me the remaining $800, which put me at 5× leverage, since $1,000 divided by $200 equals 5. I knew I’d be paying interest on the $800 I borrowed.

Once I was in the trade, the math became very clear. When the stock rose by 10%, the position value increased from $1,000 to $1,100. That gave me a gross profit of $100. Because that $100 gain was made on my $200 of equity, my return on equity was 50%.

But the leverage worked both ways. When the stock fell by 10%, the position value dropped to $900, leaving me with a $100 loss. That loss was still measured against my $200 equity, which meant I was down 50% on my capital.

I also had to factor in interest. The broker charged 6% per year on the $800 loan, which came to $48 annually. If I held the position for a full year and the stock rose 10%, my net profit after interest was only $52. That worked out to a 26% return on my $200 equity. If the stock hadn’t moved at all, I still would have paid the $48 in interest, which amounted to a 24% drag on my capital just for holding the leveraged position.

Takeaway: margin multiplies upside and downside. With $200 of equity and $1,000 exposure, a modest price swing produces big percentage moves on your cash, and interest drags that compound the risk over time.Keep that equation front of mind: margin magnifies returns, and it magnifies pain.

Practical Considerations When Trading on Margin

Traders must be aware of the unique set of practical considerations involved in margin trading. The following are some of the key factors:

Initial margin requirement

This is the percentage of the total trade value that the broker requires as a deposit to initiate a margin trade. This requirement varies between brokers and can range from 10% to 50% or more. For example, if you want to buy $1,000 worth of Tesla stock, and the initial margin requirement is 30%, you would need to deposit $300 into your margin account.

Maintenance margin requirement

This is the minimum account balance that you must maintain after the trade has been initiated. If the account value drops below this level due to losses, the broker may issue a margin call, requiring you to provide additional funds to maintain the margin. The exact maintenance margin requirement will depend on the broker, but it typically ranges from 25% to 30% of the total trade value.

Margin calls

As I've mentioned, if your investment dips below the maintenance margin, your broker will issue a margin call requiring you to deposit additional funds to meet the minimum balance. If you can’t meet the margin call, the broker may liquidate your position to cover the shortfall.

Interest rates

When you borrow funds from your broker, you'll have to pay interest on the borrowed amount. These rates can vary widely from broker to broker, so it's essential to understand these costs before opening a margin account.

Leverage

Leverage is the ability to control large amounts of a security or contract value with a comparatively small amount of capital. However, while higher leverage can magnify potential profits, it also amplifies potential losses. Leverage can be tightly controlled in certain markets. In Europe, you typically cannot get leverage of more than 30:1.

Market volatility

Given the highly volatile nature of many financial markets, particularly the FOREX and crypto markets, you must be prepared for constant fluctuations in your account value.

Risk of loss

Margin trading can lead to losses that exceed your initial investment. If a trade goes against you, you're still responsible for repaying the loan.

Broker's terms and conditions

Each broker has its own set of rules and regulations around margin trading. Traders should familiarize themselves with these to avoid surprises.

You should understand the costs and risks before engaging in margin trading. A good risk management strategy helps you avoid irresponsible margin trading.

Step-by-Step Guide to Buying on Margin

Buying on margin is simple in idea and real in consequences: you borrow from your broker to buy a bigger position. Below are the concrete steps you should follow, along with a worked example to illustrate the math.

Open and approve a margin account. Contact your broker, complete the margin account application, and read the margin agreement. The agreement outlines initial margin rules, maintenance thresholds, and the interest rate you’ll pay.

Fund the account. Deposit cash or marginable securities. These assets act as collateral for the loan.

Check the broker’s margin rules. Confirm the broker’s initial margin requirement (common in many jurisdictions: 50% or 0.50) and the maintenance margin (often 25% or higher). Also note the broker’s margin interest rate and how it usually accrues.

Calculate buying power. Use this formula:Maximum purchase = deposit ÷ initial margin requirement.Example: deposit = $5,000; initial margin requirement = 0.50.Step by step: 5,000 ÷ 0.50 = 10,000.You can buy up to $10,000 of securities because the borrowed amount is $5,000, which is $10,000 minus the $5,000 margin requirement.

Place the margin order. When you submit the buy order, select margin financing (if your platform offers this option). The broker executes the trade and records the loan.

Monitor the maintenance margin continuously. If market value falls, your equity falls and may trigger a margin call. Example: you bought $10,000 of stock financed with a $5,000 loan. If the market value drops to $7,000, then the equity is calculated as follows: Equity = market value − loan, which is $ 7,000 − $ 5,000 = $2,000.Equity percentage = 2,000 ÷ 7,000, which is 2/7 = 0.285714… therefore 28.57% (above a 25% maintenance threshold).If the market value falls to $6,000, then the equity is $6,000 − $5,000 = $1,000.Equity percentage = 1,000 ÷ 6,000 = 1/6 = 0.166666… therefore 16.67% (below 25% - margin call).

Respond to margin calls promptly. The broker may require you to deposit cash or sell positions. Interest accrues on the borrowed $5,000. Selling securities typically repays the loan first and returns any leftover equity to you. You should always factor interest into your expected return. Why? Because margin only helps if your investment return exceeds the interest and fees.

Use risk controls. Set stop losses, size positions so a single trade doesn’t jeopardize your portfolio (as we always say, risk no more than 1–2% of total capital), and prefer short holding periods to limit interest drag.

Follow these steps exactly, run the simple arithmetic before you trade, and keep an eye on maintenance ratios and interest costs. That discipline keeps margin a tool, not a trap.

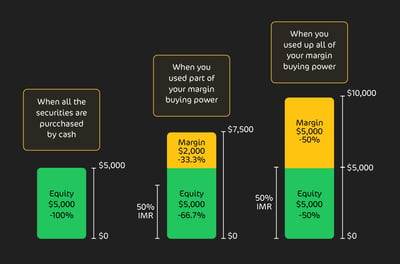

Real-world Worked Example

Look at the following graphic. If you put $5,000 into a margin account and your broker’s initial margin is 50%, your buying power is $10,000 (shown on the far right), because the broker will loan you up to the other half. If you buy $5,000 of stock, you still have $5,000 of purchasing power left.

You haven’t borrowed anything yet because your own $5,000 still covers the purchases. You only start using margin when your total purchases exceed your cash deposit. For example, buying $7,500 of stock would mean $2,500 (33% of your buying power as shown in the middle of the graphic) is financed by the broker.

Buying power isn’t fixed. It changes every trading day as the market value of your marginable securities moves, so check it before you place trades and keep a buffer to avoid accidental margin calls.

What are the key elements of margin trading?

Margin trading is built around a few core elements that determine how the loan works and how much risk you take. These usually include your margin account, the amount borrowed from the broker, and the collateral supporting the position. Understanding these basics makes it easier to manage leverage responsibly.

Minimum margin

Regulators and brokers insist that you sign a margin agreement before you can borrow. In practice, this typically involves opening a margin account (either as part of your primary account or as a separate agreement) and meeting the broker’s minimum deposit requirements. In many markets, the commonly quoted regulatory floor is $2,000, but many brokers set higher thresholds.

Initial margin

Initial margin is the portion of a purchase that you must fund yourself before the broker lends the remaining amount. A typical rule is 50%: put up $5,000 and you can buy $10,000 of stock; borrow $5,000 from the broker. You don’t have to borrow the maximum; you can use 10%, 25% or any level your broker allows, as we’ve shown. Remember: the loan accrues interest and remains on the account until it is repaid. When you sell, the proceeds are first used to pay off the loan.

Maintenance margin and margin call

The maintenance margin is the safety line you must keep above in your account; if you fall below it, your broker issues a margin call, a demand to top up your cash or sell holdings. If you ignore the call, the broker can liquidate your positions (and select which ones) without your consent. That can trigger commissions, tax events and real losses; you’re liable for any shortfall and for fees.

It’s always a good idea to determine your broker’s maintenance threshold, maintain a comfortable buffer above it, set price alerts, and be prepared to add cash quickly. Margin amplifies returns, but it also amplifies the speed at which your account can be wiped out.

What should margin investors consider?

I would always remind new traders that borrowing on margin costs you real money and requires your securities to be used as collateral. The headline cost is interest, which can materially raise your break-even point the longer a margin position stays open. That means your debt can snowball. Higher principal leads to higher interest, which in turn raises the principal again if unpaid, so the margin is best treated as a short-term tool, not a buy-and-hold strategy. The longer you sit in a margin position, the bigger the return you need just to break even after interest and fees.

Always do the math before you borrow. Your target return must exceed the margin interest plus any trading costs. If it doesn’t, you are borrowing unnecessary risk. Also bear in mind that not every security is marginable and not every platform offers margin across all products. Brokers and exchanges set their own rules, and some assets, such as penny stocks, many IPOs, and a lot of crypto listings, are commonly blocked from margin trading because of extreme day-to-day volatility.

What does “margin” mean outside trading?

Margin does not only apply to trading; the term also appears in several other financial and business contexts. Its meaning changes slightly depending on the subject, but it generally refers to a difference, buffer, or amount set aside. The examples below show other common uses of the term margin.

Accounting margin

In business accounting, margin is simply the gap between what a company sells and what it costs to run the business. Firms typically watch three margins closely because each tells a different story about profitability.

Gross margin looks at revenue minus cost of goods sold, expressed as a percentage, (Revenue − COGS) ÷ Revenue, and shows how efficiently a company turns inputs into product. Operating margin then folds in operating expenses (selling, general & admin, R&D): Operating income ÷ Revenue, which tells you how well the core business converts sales into operating profit. Net margin is the bottom-line figure, Net income ÷ Revenue, after interest, taxes and one-offs, and it shows what shareholders actually retain from every dollar of sales. Read them together and you get a clean, layered view of where profits are made and where pressure might be hiding.

Margin in mortgage lending

An adjustable-rate mortgage (ARM) gives you a fixed interest rate for a set introductory period, then lets the rate move afterwards. Lenders don’t guess the new number. They add a fixed spread (the margin) to a published index (the part that moves). The margin typically remains the same for the life of the loan; the index is what fluctuates in value.

Put simply: new rate = index + margin. So with a 4% margin on a loan tied to a 6% Treasury index, your rate becomes 6% + 4% = 10%. That’s why the index matters: if it falls, your rate falls; if it climbs, your rate rises.

Before you sign, those details determine how volatile your payments can be.

- Check which index your ARM uses.

- Check how often it resets.

- Check any caps on rate changes.

How can you manage risk in margin trading?

You can manage risk in margin trading by limiting exposure, controlling losses, and using clear rules before entering a trade. Because leverage can magnify losses as quickly as gains, disciplined risk management is essential. The methods below are practical ways to protect your capital when trading on margin.

Have a trading plan

A well-structured plan brings consistency to your trading activities and lays the groundwork for scaling up to profitable trading in a sustainable manner. An effective trading plan should include a detailed strategy for entering and exiting positions. Be sure to watch out for crucial aspects, such as entry and exit indicators, position sizing, and stop-loss placements.

From my experience, I cannot overemphasize the merits of sticking to a trading plan. If you do it right, trading can become less of a gamble and more of a calculated manoeuver, aided by rational and controlled decision-making. Losses are an inevitable part of your trading journey, but how you recover from them is key. Will you abandon your carefully crafted plans when the going gets tough?

Stop-loss orders

As I've mentioned, effective risk management is a crucial component of responsible trading. A vital part of this is the stop-loss order, a safeguard mechanism that caps losses by setting a predetermined price at which your position is sold.

Imagine you buy a Bitcoin futures contract at $500. To minimize losses, you can set a stop-loss order at 20% below your purchase price, say $400. If Bitcoin takes a dive and dips below $400, the stop-loss order is triggered. The broker offloads your contract. It's essential to note that, although your trigger point for exit is $400, the actual execution price may be lower due to market volatility. Regardless, you're ensuring that your losses are limited and controlled.

A stop-loss order acts as a self-imposed speed bump, slowing your journey toward a certain level of loss. The best part of it is that you can set it and forget it without having to be constantly vigilant.

Don’t risk more than you can lose.

Never gamble with funds you can't afford to lose. When it comes to investing, savvy investors only trade with funds they may never see again. Navigating volatile markets like FOREX and crypto is like walking a financial tightrope. You can lose your balance quickly, so it’s essential to set aside funds you are comfortable with potentially losing.

Remember this: trading should never endanger your financial well-being. Keep your trading capital separate from your essential funds. This will ensure that you can weather inevitable losses when they arise.

Take profit when you can

When good planning and fortune smile upon you, it's wise to pocket your winnings. The opposite of a stop-loss is a take-profit order, which allows you to automate the point at which you take a profit from winning trades. You can configure your account to take profit at a pre-determined level. This allows you to take profit and reduces the chances of you making an emotional decision to ride out a trade, which could turn against you. By setting a take-profit order, you're proactively managing your trading journey, ensuring that profitable moments don't slip through your fingers due to rapid market movements.

Recommended Brokers

What are the pros and cons of margin trading?

Margin trading offers both potential advantages and serious risks, so traders need to weigh both before using it. The main benefit is greater buying power, while the main drawback is that losses can grow faster with leverage. Understanding both sides helps you decide whether margin fits your strategy.

Pros of margin trading:

Leverage your capital. Margin lets you control a bigger position than your cash would allow, more exposure, bigger potential upside.

Seize more opportunities. With extra buying power, you can act on timely ideas you’d otherwise miss.

Flex both ways. Margin supports longs and shorts, so you can profit from rises and falls (shorting prominent names is a standard tactical play).

Diversify without new cash. Extra capital makes it easier to spread risk across positions, rather than concentrating your money in a single bet.

Amplified gains (and follow-on leverage). If your collateral increases, your usable leverage can expand, allowing you to scale winning trades.

Operational flexibility. Margin loans are typically open-ended until you close positions; there’s often no fixed repayment schedule like a term loan.

Efficient capital use. You use existing assets as collateral rather than tying up new capital, which can improve portfolio turnover and responsiveness.

Cons of margin trading:

Losses are magnified. Leverage doesn’t care which way the market moves, a small adverse swing can wipe out your equity far faster than in a cash account.

Margin calls force action. If your equity falls below the maintenance threshold, the broker will require additional cash or collateral, and you should have that spare capital on hand.

Brokers can liquidate without consent. If you ignore a margin call or can’t top up, the broker may sell positions for you, choosing which holdings to close and potentially crystallizing losses.

Interest stacks up. Margin is a loan. Interest accrues whether you win or lose, so the longer you hold, the higher the return required just to break even.

You can owe more than you put in. Rapid falls can leave you short of covering the loan; you’re liable for any deficit plus fees and commissions.

Volatility and liquidity risk bite hardest. In fast, illiquid moves (such as crypto crashes or thinly traded small caps), forced selling can accelerate losses and worsen fill prices.

Costs, tax events and operational headaches. Liquidations can trigger commissions and taxable events, and broker rules, notifications and timings can work against you.

What are the best strategies for trading on margin?

Margin trading presents exciting opportunities, but it's a high-stakes game that requires careful planning and execution. Here are some effective strategies to keep in mind when trading on margin:

Start slowly

Margin trading isn't a sprint. Start with a modest, manageable level of leverage, especially if you're new to margin trading. As you gain experience, you can gradually increase your margin.

Practice with demo trading

Many trading platforms offer demo or paper-trading accounts, where you can practice trading with virtual money. This risk-free environment is an excellent way to familiarize yourself with margin trading and to test and refine your trading strategies.

Don't keep positions open for too long

I can attest from my own trading career, the longer you keep a margin trade open, the more interest you'll accrue on the borrowed money. Be mindful of interest charges and consider closing positions within a short- to medium-term timeframe. You should always be aware of any additional broker fees and charges and treat them as part of your overall trading costs.

Don't risk too much on each trade

Set a limit to the percentage of your total trading capital that you're willing to risk on each trade. Most seasoned traders will tell you not to risk more than 1-2% of your capital on any single trade.Set stop-loss and take profit levels

As I've said, to manage risk effectively, make sure to set stop losses and take profit levels for every trade. This will automatically limit your losses and secure your profits.

Stay informed

Keep up to date with market news and updates. Financial markets are significantly influenced by economic indicators, geopolitical events, and even market rumors. Staying informed will help you make more educated trading decisions by staying abreast of the news and using technical analysis.

The Bottom Line

Margin trading can offer greater market exposure and the potential for amplified returns, but it also increases the risk of rapid, significant losses. As discussed, understanding how it works, choosing the right markets, and applying sound investment strategies, money management, and discipline are essential before putting capital at risk.

If you are considering margin trading, start with self-education and thorough research before committing real funds. The opportunity can be exciting, but long-term success depends on risk awareness, careful decision-making, and knowing your limits.

FAQ

Margin trading means borrowing money from your broker to control a larger position than your cash alone would allow. It can increase potential gains, but it also magnifies losses and adds interest costs.

You deposit cash or marginable assets into a margin account, and the broker lends the rest. Your deposit and purchased securities act as collateral, while your equity rises or falls with the market.

Leverage is the multiple between your own capital and your total market exposure. For example, with $200 controlling a $1,000 position, you are using 5× leverage, which boosts both upside and downside.

A margin call happens when your account equity falls below the broker’s maintenance requirement. You may need to add cash, deposit more collateral, or reduce positions quickly to avoid forced liquidation.

Margin trading can provide higher potential returns due to the larger amount of capital at play. It also allows traders to open short positions and to diversify their portfolio more broadly as part of their risk management strategy.

The risks of margin trading include the potential for larger losses, the possibility of a margin call, and the burden of interest on the borrowed funds. Traders could also face the risk of having their positions unilaterally closed by the broker if a severe market downturn occurs.

Margin trading is most suited for experienced traders who have a high risk tolerance and a deep understanding of the market. Whilst it is not generally recommended for beginners, many newbies cannot resist its attraction. In this case, traders must work carefully to a well-structured plan.

Yes, many trading platforms offer demo accounts where you can practice trading with virtual money. This creates a risk-free environment where you can learn about margin trading and test your strategies.

Yes. If the market moves sharply against you, losses can exceed the cash you originally deposited. You still owe the broker the borrowed amount, plus any interest and applicable fees.

Depending on the broker, margin trading may be available for stocks, FOREX, cryptocurrencies, futures, some ETFs, certain bonds, commodities, and some options strategies. Not every asset is marginable, especially highly volatile or restricted securities.

The biggest risks are amplified losses, margin calls, forced liquidations, and interest costs that keep building while a trade is open. Volatile markets can make those risks appear much faster than many beginners expect.

Usually not at the start. Margin trading is better suited to traders who understand leverage, risk management, and broker rules, because mistakes can become expensive very quickly when borrowed money is involved.

Yes. Brokers normally charge interest on the amount you borrow, and that cost keeps accruing while the position remains open. If your trade does not outperform that borrowing cost, your returns can shrink or turn negative.

Use smaller position sizes, keep leverage modest, set stop-loss and take-profit levels, and risk only a small part of your capital on each trade. Monitoring your maintenance margin closely also helps prevent avoidable margin calls.