Table Of Contents

- How Does Slippage Work in Real Trading?

- How Does Slippage Differ Across Financial Assets?

- What’s the Difference Between Positive and Negative Slippage?

- What Are the Main Causes of Slippage?

- Which Order Types Are Most Affected by Slippage?

- How Can I Reduce or Manage Slippage?

- What is My Broker’s Role in Slippage?

- How Does Slippage Vary by Execution Model?

- How Does Slippage Affect Risk Management?

- How Can I Test for Slippage?

- What Are the Biggest Myths About Slippage?

- Final Thoughts

The Ultimate Guide to Slippage in Trading

Slippage in trading can quietly increase your costs, distort your entries, and undermine even a solid strategy. For many traders, it shows up unexpectedly, especially in fast-moving or low-liquidity markets.

In simple terms, slippage is the difference between the price you expect when placing an order and the price you actually get when the trade is executed. In this article, we’ll explain what slippage is, why it happens, and how to manage it across different asset classes.

Slippage happens when the price you expect on an order isn’t the price you actually get, and it can work in your favor (positive slippage) or against you (negative slippage).

It’s most common in fast-moving or thinly traded markets where prices shift before your broker can execute your order.

Market orders are the most vulnerable to slippage because they execute at the next available price, while limit orders can help protect you.

Liquidity plays a major role; major currency pairs or blue-chip stocks tend to see less slippage than exotic pairs or thinly traded assets.

Time of day matters; slippage is usually higher during off-hours or when news events cause spreads to widen, or when volatility spikes.

Different brokers handle slippage differently; some let you set maximum tolerances, while others may automatically fill you at less favorable prices.

Testing slippage on a live account over a period of time helps you understand whether your broker’s execution is fair.

Smart risk management, like trading liquid markets, using limit orders, and avoiding illiquid sessions, can help you reduce the long-term costs of slippage.

How Does Slippage Work in Real Trading?

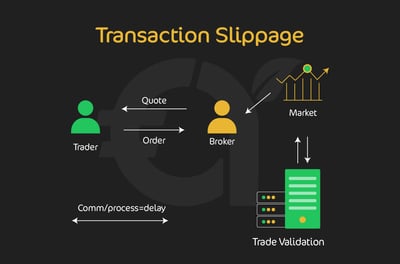

Imagine you click “buy” on EUR/USD at 1.0850, but by the time the trade executes, some minutes later, you’re filled at 1.0853. That’s a three-pip gap, which is known as slippage. On a standard lot, it costs you $30 instantly. It happens because markets don’t stand still. Liquidity, volatility, and your broker’s execution speed all play a role.

Liquidity problems happen when there aren’t enough buyers or sellers at your chosen price, or when the market moves too fast for your broker’s systems to keep up. This is when we see that your order slips to the next available level.

The diagram below illustrates the sequence of processes required for an order to be finalized. This demonstrates why it is no surprise that slippage can occur:

The same principle applies to stocks. If you try to buy Apple at $210 but rapid order flow pushes the fill to $210.50, you’ve slipped 50 cents per share.

In the crypto world, where liquidity is fragmented across multiple exchanges, the effect can be even more damaging. You could place your Bitcoin order at $65,000, but it only fills at $65,150 in a thin market, resulting in a cost of $150 per coin.

How Does Slippage Differ Across Financial Assets?

Slippage differs across financial assets because liquidity, volatility, and market structure are not the same in every market. Its real cost depends on how quickly prices move and how much depth is available when your order reaches the market. Understanding these differences makes it easier to apply risk management and judge the impact of order execution.

FOREX

You go long on GBP/USD at 1.2750 during the New York–London overlap, but volatility spikes after a surprise inflation release. Your market order fills at 1.2754 instead. That 4-pip slippage on a standard lot translates to a $40 cost.

FOREX is one of those assets that is affected by the news. When a major news announcement occurs (or even when the market opens after the weekend), price gaps appear, causing slippage.

For example, you placed a trade on Friday, and it was executed on Monday due to the price gap. This is demonstrated in the graphic below.

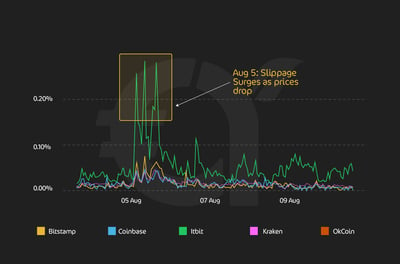

Crypto

You place a market buy on Bitcoin at $65,000 on a Sunday evening, when liquidity is thinner. By the time the crypto order executes, the price has moved to $65,300. The $300 difference per coin is slippage, and if you’re buying 2 BTC, that’s a $600 hit.

You can just imagine the potential slippage across exchanges for different trade sizes. The chart below is a hypothetical example that illustrates how price slippage increased between August 5th and 7th for BTC-USD, suggesting liquidity issues.

Stocks (and CFDs)

Imagine you want to take a long position on Nvidia stock when it’s trading at $180 per share. You place a market order to buy 50 contracts for difference (CFDs). However, right after a strong product launch announcement, trading activity on the stock market surges, and the price rushes. By the time your order is executed, the best available stock price is $180.30. Your order is filled at this higher level rather than the $180 you expected. That $0.30 gap per share represents slippage.

.webp)

In this scenario, you’ve encountered $15 in negative slippage. While this may not seem significant, it reduces your edge and can add up over multiple trades, especially in volatile markets.

Commodities

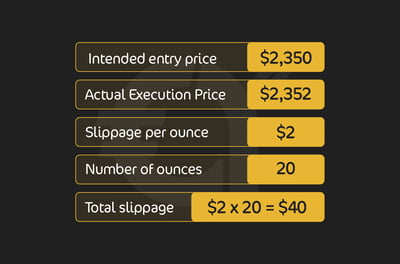

Imagine you want to go long on gold when the price is $2,350 per ounce. You place a market order to buy 20 ounces. However, during a period of extreme volatility after some bad inflation data, the commodity market moves quickly.

By the time your order is processed, the best available price has risen to $2,352. Instead of being filled at $2,350, your order is executed at $2,352. The $2 per ounce difference is the slippage.

In this case, you’ve experienced $40 of negative slippage, meaning your trade opened at a less favorable price and narrowed your profit margin.

So, the lesson across all markets is the same: the more liquid and orderly the market, the less slippage you’ll face. The thinner or more chaotic it is, the more you should expect your orders to fill at unplanned prices.

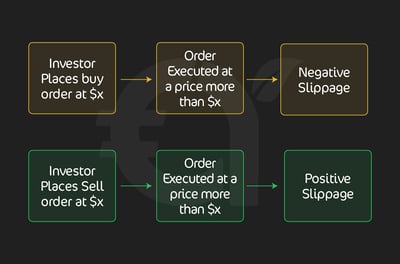

What’s the Difference Between Positive and Negative Slippage?

Positive slippage happens when your trade is filled at a better price than expected, while negative slippage means you get a worse price than planned. Both occur when the market moves before your order is executed. In practice, negative slippage tends to be more common, especially in fast markets with lower liquidity.

How do we know this? US brokers regulated by the NFA/CFTC are required to publish execution quality statistics.

On a standard lot, a four-pip slip costs you $40 before the trade even gets going.

Positive slippage, though rarer, works in your favor. Suppose you’re long EUR/USD at 1.0850, but extra liquidity drives your fill down to 1.0848. That two-pip improvement saves you $20 instantly on a standard lot.

Both outcomes are part of live trading. The key is recognizing that slippage reflects how fast markets move and how much liquidity is available at the moment your order hits. Sometimes you’ll pay a little extra, sometimes you’ll get an unexpected advantage, but over the long run, your trading strategy should be robust enough to handle either.

In our review of broker execution disclosures over the past 12 months, the most consistent pattern we saw was that negative slippage clustered around news releases and thin trading windows, while positive slippage appeared less often and usually on smaller orders.

What Are the Main Causes of Slippage?

Slippage is mainly caused by volatility, low liquidity, and delays in order execution. When prices move quickly or there are not enough orders at your chosen price, trades can be filled at a different level. The broker’s speed and market conditions together determine how large that gap becomes.

liquidity

volatility

execution speed

If you’re trading a highly liquid pair like EUR/USD during peak London hours, orders tend to fill right on time. But if you happen to be trading in a thin market, such as an exotic currency pair or a small-cap stock, the lack of buyers and sellers means your order can only be filled at the next available price.

Volatility, as we’ve indicated, adds fuel to the fire. Big events, such as a Fed rate decision or nonfarm payrolls, can move markets in seconds, creating significant gaps that push fills away from your intended entry.

Broker speed also matters. A fraction of a second in execution time can decide whether you’re slipped two pips or twenty.

Timing plays its role, too. Slippage is far more common during out-of-hours sessions, when liquidity dries up and spreads widen.

In FOREX, that could be trading during the Asian session on a pair dominated by European flows. In stocks, it’s common right at the open, when pent-up orders from overnight news flood the market. Even cryptocurrency, which trades 24/7, is not immune; weekend volumes tend to be thinner, making large orders prone to slippage.

Join a Trading Community That Moves Together

Follow top traders and learn from real strategies.

Like, comment, and engage with other investors.

Discover experts through transparent performance data.

Connect with a community built on trust and results.

Grow your knowledge while trading smarter together.

.webp)

Which Order Types Are Most Affected by Slippage?

Order types are affected by slippage differently because some prioritize execution while others prioritize price. Market orders are usually more exposed since they fill at the best available price, while limit-based orders can reduce unwanted price changes by setting stricter conditions. The actual impact still depends on liquidity and market speed at the time of execution.

Market Orders

Most exposed to slippage because they promise immediate execution at the best available price.

Speed comes at a cost: if liquidity is thin or volatility spikes, your order will be filled at the available price, often a few pips or ticks worse than expected.

Harshest slippage often occurs following news releases, when spreads widen dramatically.

Limit Orders

Guarantee your price but not your execution.

If the market gaps past your level without trading through it, your order won’t be filled.

Advantage: no slippage

Risk: You may miss the trade entirely

Stop Orders

Fall somewhere in the middle.

Once triggered, they turn into market orders, which expose them to slippage.

A buy stop above resistance can slip higher if the price gaps through your level.

A sell stop below support can slip lower if momentum accelerates quickly.

The takeaways are simple: market orders give certainty of execution but leave you open to slippage; limit orders eliminate slippage but may leave you on the sidelines; and stop orders can still slip in fast markets because they turn into market orders once triggered. Knowing when each order type is most vulnerable helps you pick the right tool for the conditions you’re trading.

How Can I Reduce or Manage Slippage?

You can’t eliminate slippage, but you can stack the odds in your favor. The first step is timing. Trade during the most liquid sessions when spreads are tight and order books are deep. For FOREX, that’s the London and New York overlap; for stocks, it’s usually mid-session, once the opening volatility has settled. Thin hours, like late in the Asian session or low-volume crypto weekends, are when slippage bites hardest.

Order choice matters, too. Market orders guarantee a fill but leave you exposed to whatever price the market serves up. Limit orders, on the other hand, ensure your price, though you risk missing the trade if the market skips past your level. Some brokers also offer guaranteed stop orders, which can lock in your exit price even in gapping conditions, though they usually come with a premium.

Finally, be mindful of significant news events. Central bank decisions, job reports, and earnings releases can move markets in seconds, creating precisely the kind of spikes where slippage is most pronounced. Unless your strategy is designed explicitly for trading those events, the safer move is to wait until volatility subsides and liquidity returns. By combining good timing, smart order types, and disciplined planning, you can keep slippage from eroding your edge.

In live market monitoring, we consistently see slippage rise sharply during the first few minutes after major data releases, which is why waiting even a short period for spreads and depth to normalize can materially improve execution.

What is My Broker’s Role in Slippage?

Your broker plays a major role in slippage because its execution rules determine how much price movement is accepted before your order fills. Some brokers apply a slippage tolerance that rejects or requotes orders if the market moves too far. That can help protect you from unwanted fills, but it may also affect how quickly your trade execution goes through.

Other brokers, however, are less flexible. They might automatically fill your order at the next available price, even if the move is well outside your expectations. In fast-moving markets or during thin liquidity sessions, this can mean a much larger loss to swallow. Some brokers also restrict the ability to set maximum slippage parameters on their platforms, further reducing your control.

This is why it’s important for you to read a broker’s execution policy carefully. How slippage is handled, whether with client-friendly safeguards or more rigid, broker-favorable rules, directly affects costs, trade precision, and your strategy’s real-world performance. When reviewing broker execution policies, we pay particular attention to whether slippage settings are on the platform or buried in legal documents, because that often determines how much control a retail trader has in fast markets.

How Does Slippage Vary by Execution Model?

Slippage varies by execution model because each broker routes and fills orders differently. Some models pass trades directly into the market, while others use internal dealing processes that can change how price movement is handled. As a result, the size and frequency of slippage often depend on the broker’s order execution setup.

Market-maker brokers

Market makers take the opposite side of client trades, meaning your orders are filled internally rather than passed directly into the wider market. Because they control execution, they can choose how much slippage they are willing to allow. As we’ve mentioned, some market makers are more flexible, allowing you to cancel if the price moves too far from your request. Others may simply fill the order at the next available price, even if it’s significantly worse.

Straight Through Processing (STP) brokers

STP brokers pass your orders directly to their liquidity providers. Slippage here is more impacted by market depth and liquidity. Many STP brokers allow you to set a maximum deviation (sometimes called “slippage control”), so if the price moves beyond your chosen band, the order is cancelled rather than executed. This gives you more control.

Electronic Communication Network (ECN) brokers

ECN brokers connect you directly to an electronic marketplace where banks, institutions, and other traders post bids and offers. Execution in this trading form is highly transparent; however, you receive the price available in the book at the moment your order is executed.

In reality, that means slippage is almost inevitable in volatile or illiquid conditions, but it’s “true market slippage,” not influenced by broker intervention. ECN models hardly ever allow you to cancel after the fact; instead, you manage risk by using limit orders.

How Does Slippage Affect Risk Management?

It should be easy to see how slippage can throw off your risk management if you don’t plan for it. A stop-loss that should have closed you at 1.1000 might actually fill at 1.1005 in a fast-moving FOREX market, turning a controlled 20-pip loss into 25 pips.

That extra hit might seem like something you can absorb, but repeat it over dozens of trades, and it adds up quickly. Scalpers feel this pain the most because they’re chasing small, frequent gains. A few pips of negative slippage can wipe out the edge of a strategy that relies on tight stops and fast exits.

Swing traders, with wider targets and stops, are less affected, but they still need to be keenly aware of it, especially when holding through volatile events.

The best approach is to build slippage into your risk model. If you’re willing to risk $100 per trade, size your position as if slippage might push that to $110 or $120. It’s a small cushion that keeps you from breaking your own rules.

In the long run, treating slippage as part of the cost of doing business helps you stay disciplined and keeps your capital safe when markets move faster than your orders can keep up.

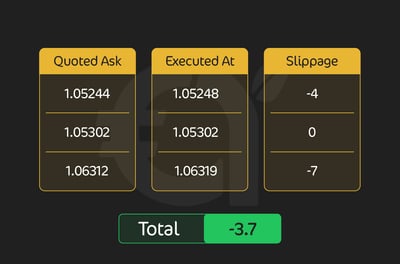

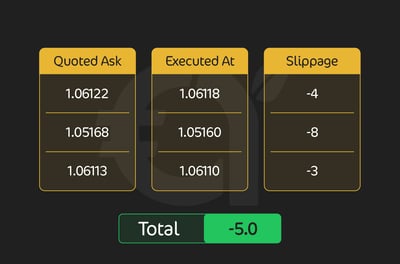

How Can I Test for Slippage?

You may wonder whether your broker is treating you fairly when it comes to slippage. The best way to know for sure is to gather data in a live account. You can do this as a one-off test, or, better yet, make it part of your ongoing trading routine.

Here’s how it works:

Buy slippage = quoted ask price – execution price

Sell slippage = execution price – quoted bid price.

For example, take three buy-side trades:

And three sell-side trades:

You then calculate the average slippage across a large number of orders, ideally over several weeks and across multiple markets. This way, you’ll see if your broker is giving you a crack at fair execution.

If everything is fair, you should expect positive and negative slippage to balance out, averaging close to zero. But if you find that negative slippage is showing up much more often, that’s a problem of which you need to be aware.

Running this kind of test costs money because you’re trading live, but it’s well spent, especially if you trade frequently or in large volumes. Over time, it can save you from trading with a broker who is not working in your best interests.

What Are the Biggest Myths About Slippage?

The biggest myths about slippage are that it is always broker manipulation, always negative, or completely avoidable. In reality, slippage is a normal part of market execution when prices move or liquidity changes. Understanding that helps traders manage expectations and build better risk management habits.

Myth 1: Slippage only works against you

Reality: Positive slippage exists, too. You can get a better price than requested when liquidity lines up in your favor. Traders often remember the bad fills and overlook the good ones.

Myth 2: Slippage means your broker is cheating you

Reality: While shady brokers exist, most slippage comes from fast-moving markets and order book depth and liquidity conditions. It’s usually not manipulation.

Myth 3: Slippage can be avoided entirely

Reality: Slippage is a common occurrence in every market, including FOREX, stocks, crypto, and more. Understanding these realities turns slippage from a mysterious threat into just another cost of doing business in the markets.

Final Thoughts

Slippage in Trading is something every trader needs to understand, because it can directly affect execution quality, trading costs, and overall performance. Whether you trade FOREX, Crypto, or Stocks (and CFDs), slippage becomes more likely during periods of low liquidity, high volatility, or major news releases.By using the right order types, timing your entries carefully, and factoring slippage into your risk management, you can reduce its impact and make smarter trading decisions. Track it, plan for it, and treat it as part of your strategy, not just an unpleasant surprise.

FAQ

Slippage is the gap between the price you expected and the price you actually received when the order was filled. It usually appears when markets move quickly or liquidity is thin.

No. Slippage can be negative, costing you money upfront, but it can also be positive, giving you a better entry or exit than expected.

Market orders are the most exposed because they guarantee execution at the next available price. Limit orders avoid slippage but risk not being filled at all.

High-impact events, such as Federal Reserve rate decisions or jobs data, trigger sharp moves and dry up liquidity. Orders hit the book at a time when prices are jumping every second.

In FOREX, multiply the pip difference by the pip value and lot size. In stocks or crypto, it’s simply the difference in price per unit times your position size.

Yes, scalpers are usually hit harder because they aim for small moves and use tighter stops. Even a small bad fill can remove much of their edge, while swing traders often have more room.

Reputable, regulated brokers don’t. Most slippage is caused by market conditions and execution speed, not manipulation. That said, unregulated brokers may play games with fills.

Trade during more liquid hours, avoid entering during major announcements, and use limit orders when price control matters more than immediate execution. It also helps to choose a broker with clear execution policies.

No, slippage can be negative or positive. Negative slippage gives you a worse fill than expected, while positive slippage gives you a better price.

The main causes are volatility, low liquidity, and execution delays. Slippage becomes more likely when prices move fast, spreads widen, or there are not enough orders at your chosen price.

Market orders are usually the most exposed because they prioritize execution over price. Stop orders can also slip after they are triggered, since they turn into market orders in fast markets.

Major news can move prices in seconds and reduce available liquidity at each price level. That makes it harder for orders to fill where you expected, especially right after the release.

Yes, slippage can happen in any market. Its size depends on liquidity, volatility, and market structure, which is why thin crypto trading or fast stock openings can produce larger price gaps.

Calculate the difference between your expected price and your fill price, then multiply it by your position size. In forex, that means converting the price gap into pips and applying pip value.

Yes, broker execution rules can affect how slippage is handled. Some brokers allow more control over price deviation, while others may fill orders at the next available price in fast conditions.

Track your quoted price and actual execution price over many live trades, then compare the results over time. If negative slippage appears far more often than positive slippage, review the broker more closely.